WELCOME TO LIVING LIES DEFEND THE FORECLOSURE KEEP YOUR HOME!!! Over 17,000,000 Visitors Most of the claims that use "securitization" as a foundation are FALSE!! That means they have no right to administer, collect or enforce any debt, note, mortgage or deed of trust.And THAT means you can successfully challenge foreclosures AND pursue damages against those who make false claims.…[...]

Continue Reading

Continue Reading

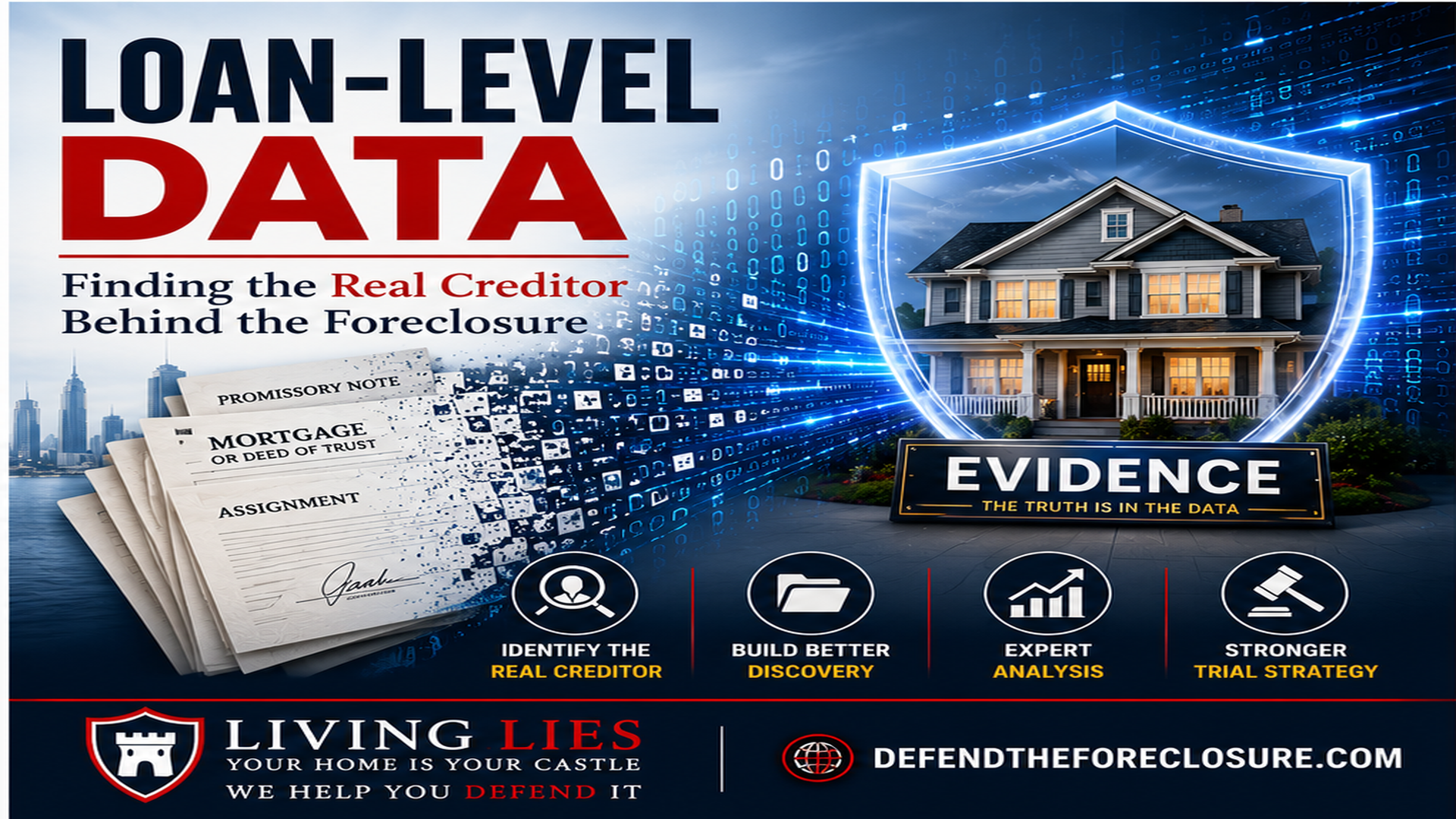

How Loan-Level Data Can Stop a Foreclosure

Jul 21, 2026

Discovering the Real Creditor Before You Lose Your Home Here's how loan level data in foreclosure defense can stop a sale; read on. For years, foreclosure litigation has focused on documents that appear in the public record. The promissory note. The mortgage or deed of trust. Recorded assignments. Affidavits signed by loan servicers. Declarations stating that someone reviewed business records.…[...]

Discovering the Real Creditor Before You Lose Your Home Here's how loan level data in foreclosure defense can stop a sale; read on. For years, foreclosure litigation has focused on documents that appear in the public record. The promissory note. The mortgage or deed of trust. Recorded assignments. Affidavits signed by loan servicers. Declarations stating that someone reviewed business records.…[...]Continue Reading

Emergency Motions to Stop a Foreclosure Sale

Jul 16, 2026

A Homeowner's Guide to Immediate Court Relief Few events create more fear than receiving notice that your home will soon be sold at foreclosure. For many homeowners, the first reaction is panic. Phone calls are made. Modification applications are rushed to the servicer. Internet searches begin late into the night looking for one simple answer: "How do I stop the…[...]

A Homeowner's Guide to Immediate Court Relief Few events create more fear than receiving notice that your home will soon be sold at foreclosure. For many homeowners, the first reaction is panic. Phone calls are made. Modification applications are rushed to the servicer. Internet searches begin late into the night looking for one simple answer: "How do I stop the…[...]Continue Reading

Preliminary Injunction in Foreclosure Cases

Jul 14, 2026

How to stop a Foreclosure sale For many homeowners, obtaining a Temporary Restraining Order (TRO) feels like crossing the finish line. The foreclosure sale has been stopped. The immediate crisis has passed. Everyone can finally breathe. Unfortunately, that is usually only the beginning. A TRO is designed to preserve the status quo for a very short period of time. It…[...]

How to stop a Foreclosure sale For many homeowners, obtaining a Temporary Restraining Order (TRO) feels like crossing the finish line. The foreclosure sale has been stopped. The immediate crisis has passed. Everyone can finally breathe. Unfortunately, that is usually only the beginning. A TRO is designed to preserve the status quo for a very short period of time. It…[...]Continue Reading

evidence expert witness Fabrication of documents foreclosure defenses Foreclosure Questions legal standing Quiet Title

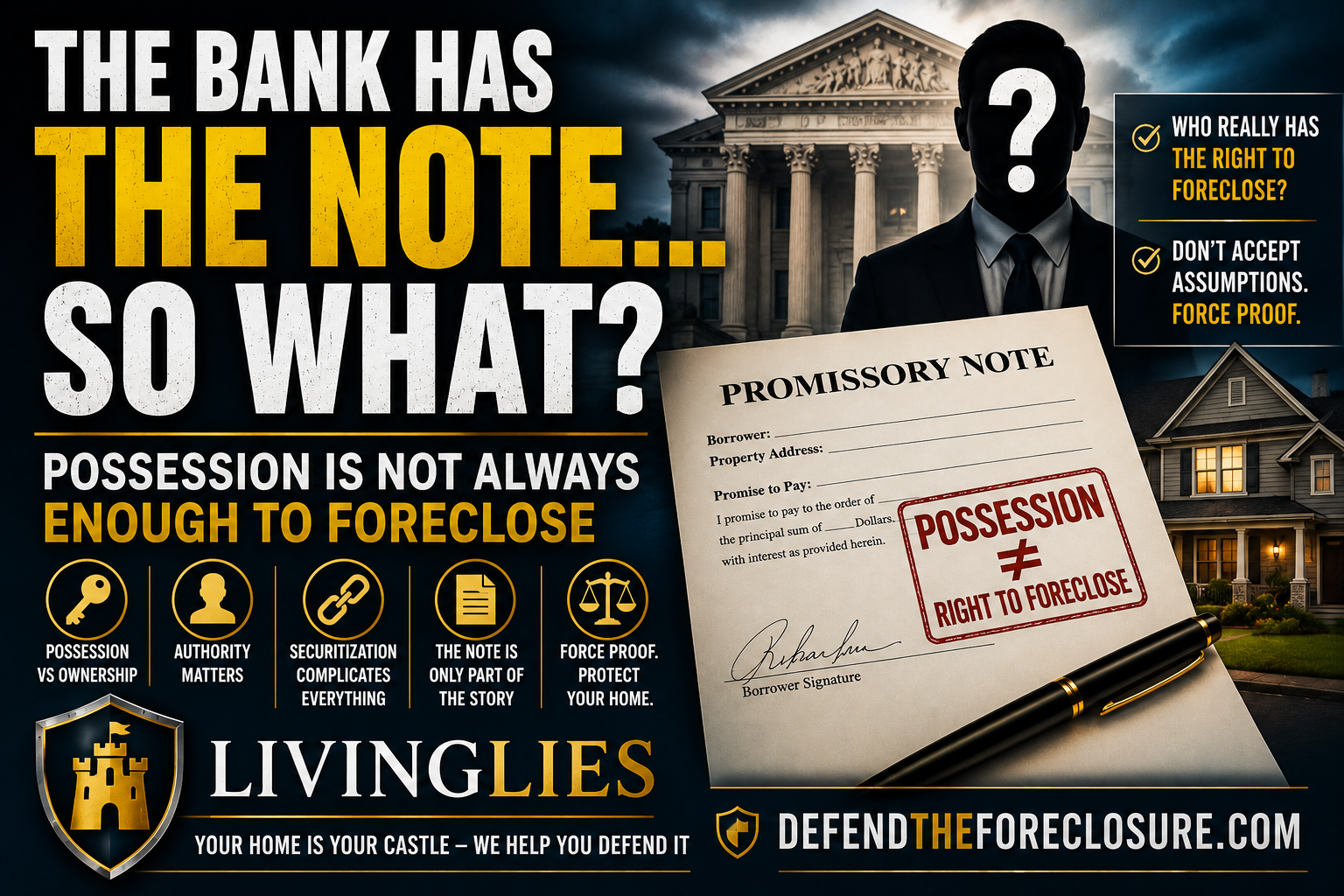

Possession of the Note Is Not Proof of Ownership

Jul 9, 2026

By Lance Denha esq. and Donna Steenkamp For more than twenty years, we have been saying possession of the note is not proof of ownership. This is something that many courts are only beginning to recognize. The foreclosure industry has successfully convinced courts to ask the wrong question. Instead of asking: "Who actually owns the debt?" many foreclosure cases begin…[...]

By Lance Denha esq. and Donna Steenkamp For more than twenty years, we have been saying possession of the note is not proof of ownership. This is something that many courts are only beginning to recognize. The foreclosure industry has successfully convinced courts to ask the wrong question. Instead of asking: "Who actually owns the debt?" many foreclosure cases begin…[...]Continue Reading

One of the most common statements heard from homeowners facing foreclosure is: "I wish I had acted sooner." Unfortunately, many homeowners do not realize how quickly foreclosure timelines can move until a sale date has already been scheduled. The notices arrive. The servicer refuses to answer meaningful questions. The foreclosure attorneys continue moving forward. And suddenly the homeowner is staring…[...]

One of the most common statements heard from homeowners facing foreclosure is: "I wish I had acted sooner." Unfortunately, many homeowners do not realize how quickly foreclosure timelines can move until a sale date has already been scheduled. The notices arrive. The servicer refuses to answer meaningful questions. The foreclosure attorneys continue moving forward. And suddenly the homeowner is staring…[...]Continue Reading

Quiet Title: How To Challenge Pretend Lender Claims

Jun 16, 2026

Continue Reading

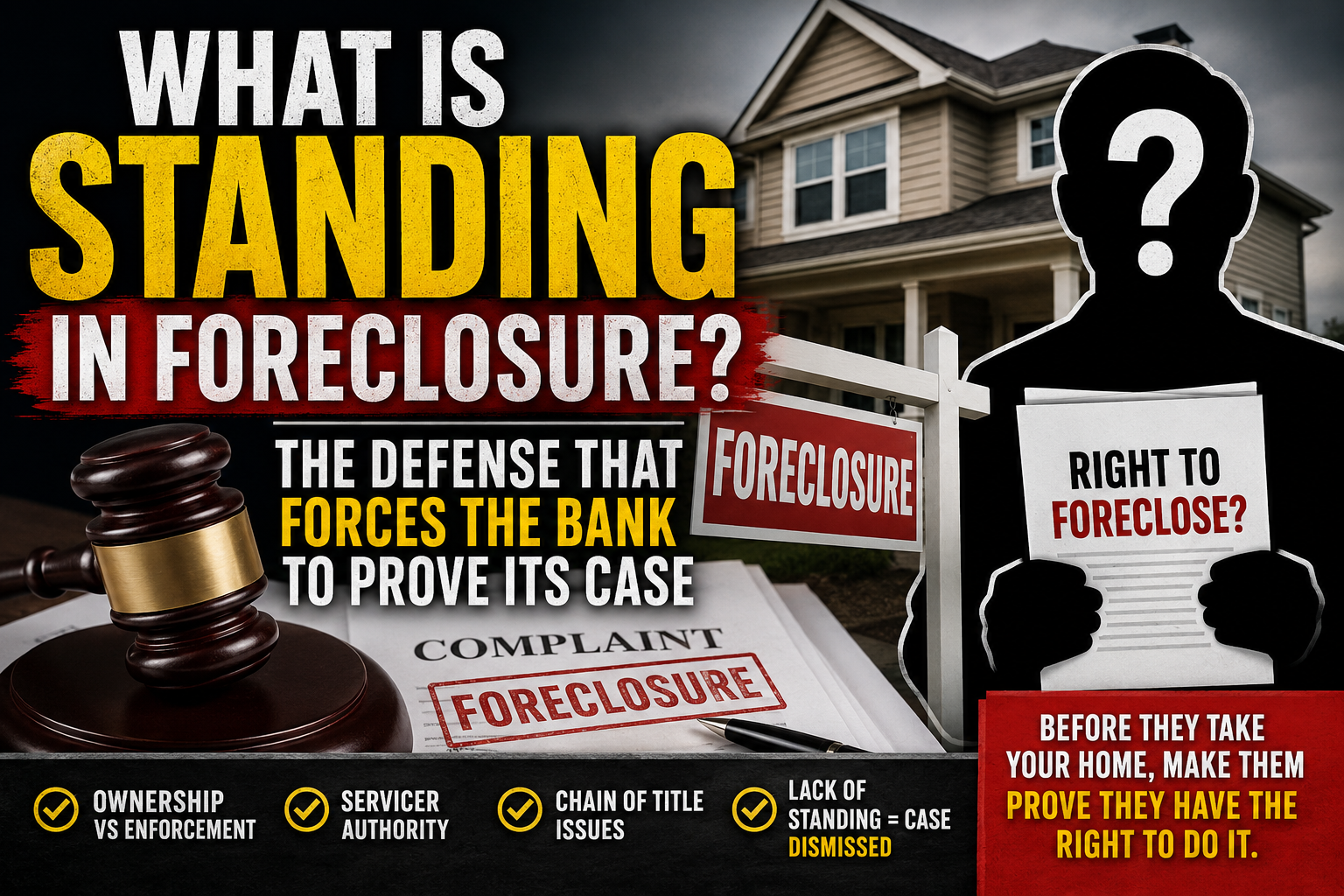

Learn how to challenge legal standing in your foreclosure defense. By now, most homeowners who have spent any time researching foreclosure defense have heard the word "standing." But knowing that standing in foreclosure matters, and knowing how to challenge standing successfully, are two different things. Many homeowners correctly identify standing as an issue but then make a critical mistake. They…[...]

Learn how to challenge legal standing in your foreclosure defense. By now, most homeowners who have spent any time researching foreclosure defense have heard the word "standing." But knowing that standing in foreclosure matters, and knowing how to challenge standing successfully, are two different things. Many homeowners correctly identify standing as an issue but then make a critical mistake. They…[...]Continue Reading

One of the most common statements heard in foreclosure courtrooms across America is: "We have possession of the note." For many judges, lawyers, and homeowners, that statement ends the discussion. The assumption is simple: If the foreclosing party has possession of the original note, it automatically has the right to foreclose. But that assumption is often wrong. Possession of a…[...]

One of the most common statements heard in foreclosure courtrooms across America is: "We have possession of the note." For many judges, lawyers, and homeowners, that statement ends the discussion. The assumption is simple: If the foreclosing party has possession of the original note, it automatically has the right to foreclose. But that assumption is often wrong. Possession of a…[...]Continue Reading

Read this 12 step Foreclosure Defense guide carefully because most homeowners lose before they ever walk into court. Not because the bank proved its case. Not because the servicer proved ownership of the debt. Not because a judge carefully reviewed every transaction involving the loan. They lose because they assume the foreclosure paperwork must be true. That assumption will cost…[...]

Read this 12 step Foreclosure Defense guide carefully because most homeowners lose before they ever walk into court. Not because the bank proved its case. Not because the servicer proved ownership of the debt. Not because a judge carefully reviewed every transaction involving the loan. They lose because they assume the foreclosure paperwork must be true. That assumption will cost…[...]Continue Reading

evidence expert witness Fabrication of documents foreclosure defenses Foreclosure Questions legal standing

What Is Standing in Foreclosure? The Defense That Works

Jun 2, 2026

If there is one issue that can change the direction of a foreclosure case, it is standing. It is a defense we help homeowners use the most and it works. Here at LivingLies we talk about it a lot but realize not everyone understands what are Legal Standing foreclosure defenses. Most homeowners never hear the word “standing” until they are…[...]

If there is one issue that can change the direction of a foreclosure case, it is standing. It is a defense we help homeowners use the most and it works. Here at LivingLies we talk about it a lot but realize not everyone understands what are Legal Standing foreclosure defenses. Most homeowners never hear the word “standing” until they are…[...]Continue Reading

Search Our Blog

Categories

Contact Our National Headquarters Phone: 844-583-5339

Connect with us

Contact Our National Headquarters

- 844-583-5339

- Available 24/7

-

200 S. Andrews Ave. Ste. 604

Ft. Lauderdale, FL 33301